As more Governors open their states for business, and political rhetoric escalates, investors are asking – What’s Next? Since our last (longer) market update, the US has “flattened the curve,” US equity markets are substantially up from their March 23rd lows, and many conversations have moved to discussing when/how to re-open the US economy & the impact of those decisions on healthcare & the markets.

Our view here is not to say that it is or is not a good idea to be re-opening the economy. Clearly, with historically, devastatingly large unemployment figures, the sooner we can get business back open, the better, but we also want to make sure that businesses can re-open safely and that the US can avoid a second wave of escalating cases & deaths. The ultimate answer would be made clearer if we had more improved testing & tracing on a national level, but at this point, that is not imminent, and by any estimate, we are still a ways away from levels recommended by experts.[1]

So as States start to re-open and businesses follow suit, with so much still up-in-the-air, at US Advisory Group, we are still largely in the ride-it-out mentality. Having said that, we have more information today than we did only weeks ago, and we will continue to use that information to make intelligent portfolio decisions. There are some industries that are getting hit harder than most and yet others that have shown greater resilience, and we are continuing to dial our portfolios in to reflect that reality. We will focus our investing on companies that we feel are most resilient and show the best value for long-term investment. For instance, research and development in many technology companies has not missed a beat. Healthcare research, cloud based computing and online retailers are also spaces we favor. We feel manufacturing will return with the opening of non-essential businesses, but companies who proved savvy enough to transfer their operations towards making essential supplies in the past two months have shown an edge.

We like how our portfolios have performed both on the downside when the market was getting hit, and as the market began a recovery in later March & April. With volatility still at historically high levels, we are continuing to favor our core strategies. Specifically, we still believe dividend-producing equity is important; we like internationals as a hedge in the event the US equity market lags a global recovery; and our fixed income positions and diversified bond portfolios have served us quite well year-to-date.

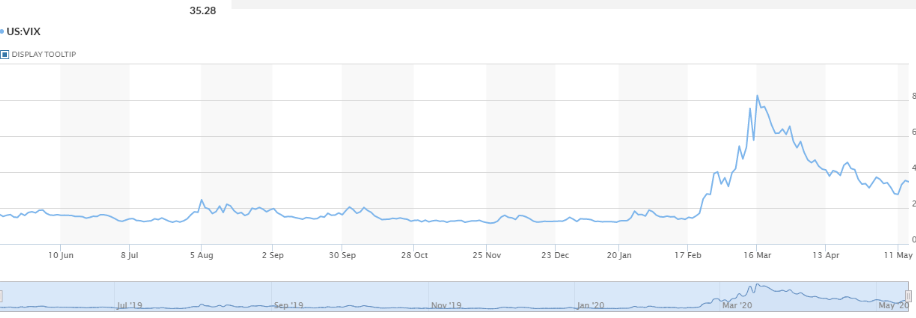

In illustration of volatility, see today’s chart (5.14.20) of the US CBOE Volatility Index (VIX):

Dramatically down from the peak, but still at quite elevated historic levels, almost 3x the historic average from 12.31.19. [2]

If the US *does* experience a “second wave” we have evidence in our portfolios that we can ride through the volatility, and when another therapeutic is announced, or a vaccine, or some other tangible positive piece of data emerges, we want to be in a position to catch the market bounce when it happens.

In the meantime, we, as always, appreciate the faith and trust our clients put in us, and we have seen that borne out in portfolios that are working through this time! As we have referenced in the last few weeks, you can expect to see enhanced active-management strategies deployed inside our portfolios, as being more-and-more selective about the specific underlying assets and sectors is key to getting the most out of the market opportunities we expect to see as the market stabilizes and the economy begins its long recovery.

The final point to make concerns the political landscape: since Bernie Sanders ended his campaign on April 8th and with Joe Biden now the (presumptive) nominee, the already-noisy political scene has been getting louder & louder. This, as we all probably assume, is only going to get worse between now and November. It is important to recognize that, historically, the market & intelligent investors care less about political rhetoric than Cable News does. We know it is not easy to block out the political news (not that you should, necessarily), especially when we are stuck at home. But for long-term investors, it is important to maintain separation between what is happening on Cable TV and how the markets are moving.

If I have said it once, I have said it a thousand times by now – the market and the economy are two different things. Sure, they are related, but as we have seen even just in the last few weeks, just because the economy is essentially re-starting from zero (in some – NOT ALL aspects!), that doesn’t mean the market is going to mirror the economy.

So hang in there – we are here for you, we are here with you. Thank you to all who have reached out with appreciative words, and thank you to those who haven’t, whose support & trust we know we have earned, and continue to earn, each day!

I hope you all stay healthy & safe, and our next update will be here soon!

[1] https://www.factcheck.org/2020/05/how-many-covid-19-tests-are-needed-to-reopen/